How blind boxes, trading cards, and cross-brand collaborations reveal what your licensing royalty structure wasn’t built to handle

Blind boxes, trading cards, mystery packs, and viral cross-brand collaborations are the fastest-moving licensing formats in the market today. But they weren’t designed with the traditional licensing royalty structure in mind. They combine multiple IPs in a single SKU, assign variable perceived value per unit, and generate active secondary markets that per-unit models were never built to track.

When a cross-brand collaboration sells out in 48 hours, or a blind box series drives secondary-market prices well above retail, the royalty infrastructure underneath it is either capturing that value or missing it. Most are missing it because the contractual and operational frameworks were built for a world that no longer describes the market.

This isn’t a marketing curiosity. It’s a revenue protection and growth problem that demands an IP licensing model built for the market that actually exists, not the one for which these agreements were drafted.

What makes blind boxes, trading cards, and cross-brand collaborations royalty-hostile

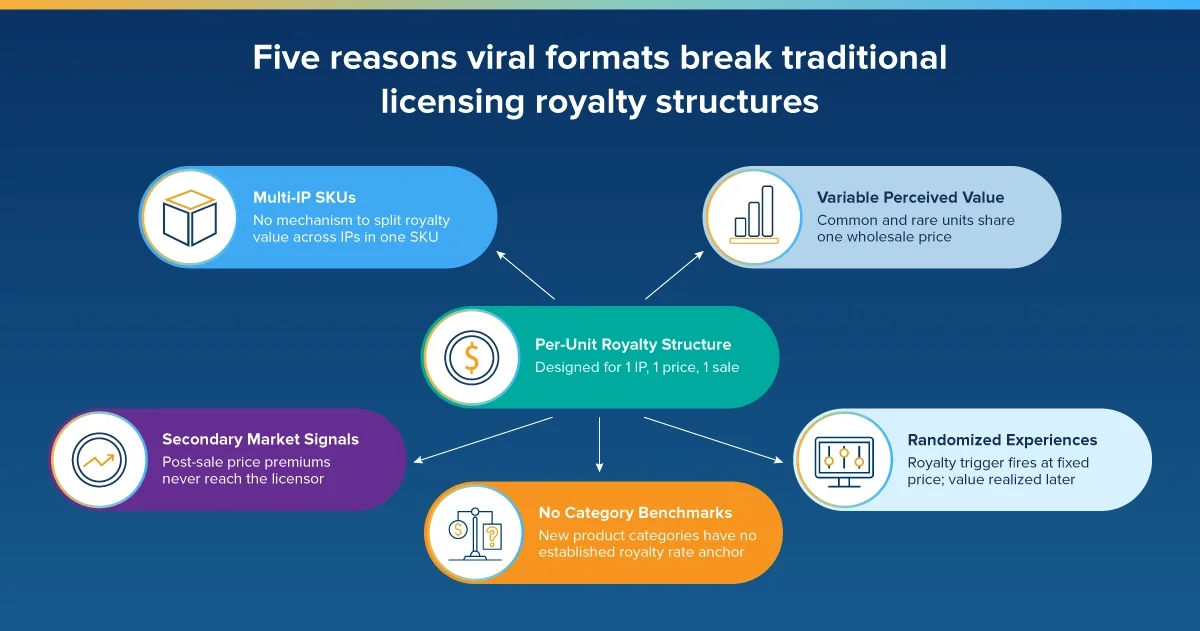

Traditional per-unit royalty structures were designed for a simple equation: one product, one IP, one price, one transaction. Viral formats break every variable in that equation simultaneously. Five structural characteristics make them hostile to legacy royalty logic.

1. Multi-IP SKUs

A single product containing two or more licensed properties requires royalty attribution at the component level. Per-unit structures assign a single rate to the whole product, with no native mechanism for splitting value across IPs sharing the same SKU. This is the most common challenge in new licensing deals right now, and its prevalence is increasing. Revenue often rises when IPs are combined because the product appeals to multiple consumer segments. But the problem is two-fold: perceived value per IP is subjective rather than objective, and larger multi-IP products are frequently not itemized at the SKU level, a gap that only surfaces during audit.

2. Variable perceived value

In a blind-box series, a common figure and a rare figure share the same wholesale price but have radically different consumer values. A royalty model built on wholesale price captures neither rarity nor demand signal. The gap between what the consumer paid and what the royalty calculation reflects is real; it’s just not visible until someone looks for it.

3. Secondary market price signals

When a blind box rare sells significantly above retail on a secondary platform, that premium represents genuine IP value the licensor’s royalty calculation never sees. Royalties are collected on the first sale of the IP product. Everything that happens downstream, including resale, grading, and secondary-market appreciation, accrues to collectors and platforms, not to licensors, unless the agreement explicitly addresses it.

4. Randomized consumer experience

Mystery packs separate the purchase decision from the value received. This creates both a royalty timing problem and a valuation problem: the royalty trigger (the sale) fires at a fixed price, but value realization (the unboxing, the secondary sale) happens later, often at a materially different price point. Per-unit structures capture the trigger. They don’t capture the value.

5. Category expansion without benchmarks

When a brand extends into a product category with no established royalty benchmark, the per-unit rate has no comparable value to serve as an anchor. Ad hoc negotiation in that context rarely favors the licensor. Without a defined rate-setting methodology, the licensor is negotiating against the licensee’s numbers with none of their own.

Five reasons viral formats break traditional licensing royalty structures

Where does your royalty structure break down?

The royalty-hostile characteristics above create specific, identifiable failure points in the way most licensing agreements are currently written and administered. The blind box model is the clearest stress test, but every failure point it exposes applies equally to trading cards, mystery packs, and the next viral format yet to emerge.

The wholesale price ceiling

Fixed-percentage royalties tied to the wholesale price lack a mechanism for responding when secondary-market prices signal that consumer-perceived value has increased. The royalty becomes a floor, not a measure of actual value captured. When a product cycle accelerates, that floor stays fixed while the market moves on.

Minimum guarantees and flat structures miss inflection points

When market growth accelerates rapidly, flat structures do not capture the upside. The inflection point passes, and the revenue gap widens. And because most royalty reconciliations happen quarterly, by the time the data surfaces, the period has already closed.

Channel and field-of-use blind spots

Legacy agreements create gaps when products migrate to online marketplace sellers, social commerce, and creator stores without recalibrated royalty accounting. This is a reporting and audit issue in active deals. Trademark integrity is also at stake once third-party ecommerce sellers enter the distribution chain.

The attribution gap in multi-IP products

When multiple IPs share a SKU, per-unit royalties require an attribution decision that most contracts do not specify. That gap becomes a dispute waiting to happen. Imagine a product that features multiple titles from a franchise. The highest-value IP, the one driving purchase intent, is the original film. But the product is loaded with elements from the sequels. Under an equal-weight royalty model, the product is valued uniformly across all titles, regardless of which IP actually moved the consumer to buy.

I believe this is the most underappreciated structural problem in multi-IP licensing today. The absence of an attribution methodology systematically disadvantages the IP with the highest consumer pull.

Cross-brand complexity

Cross-brand deals add another layer of complexity. When a single licensor owns both IPs, there is typically no empirical methodology for attributing value between them, and it defaults to internal negotiation, driven more by intuition than data. From my perspective, that process will hold provided the resolution is explicitly memorialized in the legal agreement. But it has no external defensibility when a licensee challenges the calculation.

When multiple licensors are at the table, the challenge multiplies. Rate structures and audit rights must be agreed upon by every IP holder, and the complexity of doing that at scale is one reason the problem persists. It’s simply easier to apply equal weighting and move on.

A framework for royalty models that can handle these formats

The following framework is not format-specific. It applies whenever a new product exhibits the royalty-hostile characteristics described above, which means it will remain relevant as new viral formats emerge. The goal is not to predict what comes next. It’s to build the infrastructure to handle it.

1. Component-level attribution before contract execution

Before a multi-IP SKU deal closes, define in writing what percentage of royalty value each IP contributes, under what formula, and what triggers a renegotiation if the commercial profile changes. This requires building a company-approved guidebook for assessing IP value in multi-IP products, delineated by product category. That guidebook is the first concrete step any licensor should take toward a more data-aware royalty model. Without it, every attribution decision is a judgment call made under pressure to negotiate.

2. Tiered royalty structures that respond to rarity

Royalty rates should be tiered by rarity: common, uncommon, rare, and ultra-rare. The contract must define those tiers, who controls the rarity ratio, and what audit rights the licensor retains over that mix. Regarding rarity control, the licensee should not unilaterally set the ratios. If they do, the licensor has no meaningful recourse. The licensor should, at a minimum, specify a contractual range within which the licensee must operate, and audit rights should attach to that range.

3. SKU-level reporting as a contract obligation

Require SKU-level reporting for all variable-value product lines. This is not optional for formats where rarity, variant, or packaging configuration materially affects value. Quarterly summaries at the product family level obscure the data that matters. SKU-level visibility is the second concrete step toward a functional royalty model for these formats.

4. Rate benchmarks for category expansion

For brand extensions outside traditional product categories, specify a rate-setting methodology in the agreement, such as the benchmark, comparables, or process, rather than defaulting to ad hoc negotiation. The licensor who enters a new category with a defined framework negotiates from a stronger position than one who is setting rates reactively.

5. Retailer and channel relationships as a revenue bridge

The third concrete step is less contractual and more relational: build working relationships with retailers that help connect the gap between the royalty-bearing sale by the licensee and the final consumer purchase of the IP product. Secondary revenue is currently lost across all IP products, not just multi-IP formats. Royalty is collected on the first sale. The consumer premium, social lift, and secondary-market appreciation don’t flow back to the licensor under a standard first-sale structure.

Closing that gap requires contractual language and channel-level data access that most licensing teams don’t have.

Three concrete steps for the next 12 months

- Develop a company-approved guidebook for assessing IP value in multi-IP products, delineated by product category. This is the foundation. Without a documented methodology, every attribution decision is made ad hoc, under pressure, with no defensible basis.

- Require SKU-level reporting as a standard contract obligation for all variable-value and multi-IP product lines. If you can’t see the rarity distribution, you can’t audit it.

- Invest in retailer relationships that bridge the gap between the licensee’s first sale and the consumer purchase. Secondary revenue recovery starts with visibility. Visibility starts with those relationships.

Does your licensing infrastructure support this framework?

A framework without the licensing infrastructure to enforce it is a negotiating position. Most royalty management platforms were built for a per-unit, quarterly-reporting world. The gap between what these formats demand and what most licensors currently operate generates disputes and unrecognized revenue.

Build a single source of truth

Integrate sales and marketplace performance data into a unified licensing platform. The key metrics for these formats include volume, effective price per unit, sell-through velocity, SKU-level royalty accruals, secondary-market price multipliers, and rarity-tier distribution. Without a single source of truth for all of those signals, audit readiness is aspirational rather than operational.

Require standardized reporting templates for randomized product lines as a contract obligation. Embed audit triggers with defined frequency and scope. Maintain sufficient granularity to defend royalty calculations when a licensee disputes a rarity ratio, because that dispute will come.

Automate what manual processes can’t scale

Automation and agentic AI have a direct application here: compliance monitoring, royalty reconciliation, anomaly detection, and continuous stress testing of royalty models against real market data. Surface ambiguous rights usage. Flag outlier channels. Alert on secondary market pricing thresholds that trigger escalator provisions. This is the operational infrastructure that separates a royalty model that scales from one that requires constant manual intervention.

Build vs. buy vs. partner

For a mid-size licensor looking to close the capability gap in the next 18-24 months, the partner path is the most pragmatic. It carries no cost of goods sold, avoids the time and capital required to build proprietary systems, and gives immediate access to capabilities that are otherwise difficult to develop in-house.

The ability to define and track weighted IP value per product is often lacking when licensors bring blind-box or trading-card deals to market. That is the capability to prioritize.

For licensing teams that have outgrown what their current systems were built to handle, solutions like Vistex become operationally relevant as the infrastructure layer that enables sound contract practice to be enforced at scale.

Is your licensing royalty structure built for what comes next?

Blind boxes, trading cards, cross-brand collaborations, and category-defying brand extensions aren’t outliers. They are the leading edge of where licensing is going. The royalty-hostile characteristics they share will not disappear when these specific formats cycle out. The next viral format will bring the same structural problems.

The licensing royalty infrastructure underneath your deals is either built for this market, or it isn't. Stop treating viral and non-standard formats as exceptions to your royalty model. Start treating them as a stress test that proves which one is true.

Explore more related resources

Get the latest news, updates, and exclusive insights from Vistex delivered straight to your inbox. Don’t miss out—opt in now and be the first to know!